Welcome to Memorandum Deep Dives. In this series, we go beyond the headlines to examine the decisions shaping our digital future. 🗞️

This week, we're digging into the question that rattled Wall Street at the end of June. For nearly two years, the formula for AI-era investing was simple: the more a company spent on chips, data centers, and computing capacity, the more the market rewarded it. Then, in a single volatile week, some of the biggest names in technology sold off sharply, and the old formula suddenly looked less reliable.

The numbers involved are hard to overstate. Goldman Sachs expects roughly $7.6T to flow into AI infrastructure by 2031, and the four biggest spenders alone are set to pour more than $450B into capital expenditure this year. Yet only about 3% of U.S. households currently pay for an AI service, and most corporate pilots have yet to show up in the bottom line. Something in that equation deserves a closer look.

So we followed the money. What we found is a system far more tangled, and far more interesting, than the headline figures suggest. It doesn't mean the AI boom is a mirage, but it does change how you should read every earnings report, every mega-deal, and every market wobble between now and the end of the decade.

Meet your next hire in as little as five days.

The selloff that changed the conversation

For nearly two years, the easiest way for a technology company to convince investors it was on the right side of the AI boom was to spend more money. Announcing another data center, ordering more AI chips, or raising capital expenditure was often enough to lift a company's valuation. The assumption behind that enthusiasm was simple: whoever built the infrastructure first would eventually capture the customers.

In the final week of June 2026, that assumption began to change briefly. The Nasdaq Composite fell nearly 3% over the week, dragging some of the market's biggest AI beneficiaries lower with it. Meta and Microsoft slipped into bear market territory, NVIDIA lost about 4%, and SpaceX, only weeks removed from one of the year's biggest public offerings, fell 16% in a single session. The selling spread into Asia as South Korean technology giant Samsung Electronics and chipmaker SK Hynix also declined. Analysts pointed to stretched valuations rather than a single piece of bad news, suggesting investors were reassessing something broader than a single earnings report or product launch.

The shift was subtle but important. For the first time since generative AI became Wall Street's favorite investment story, markets appeared to be asking whether spending alone was still enough. The technology itself continues to improve at a remarkable pace, and companies remain committed to building ever larger AI systems. What changed was the conversation around those investments. Investors are increasingly looking beyond the size of the buildout and toward the businesses and consumers expected to pay for it.

That question has become difficult to ignore because the scale of spending has few precedents. Goldman Sachs estimates that technology companies will invest roughly $7.6T in AI infrastructure through 2031, largely in data centers, networking equipment, and the specialized chips needed to train and run increasingly capable models. The four largest cloud providers, Microsoft, Alphabet, Amazon, and Meta, are together expected to spend more than $450B on capital expenditure during 2026 alone. Alphabet has guided to between $175B and $185B in spending this year, illustrating just how aggressively hyperscalers, the companies operating the world's largest cloud platforms, are expanding computing capacity. Yet the customer base supporting those investments remains considerably smaller.

Millions of users, few paying customers

Consumer adoption has been impressive in terms of awareness and experimentation, but paid usage tells a more restrained story. Bank of America Institute found that only about 3% of American households paid for an AI service during the early months of 2026, spending a median of roughly $20 each month. Millions of people now use AI tools through search engines, smartphones, and workplace software, yet relatively few have become paying subscribers. The technology has become widely visible long before it became a routine household expense.

Businesses present a similar picture, although for different reasons. Corporate interest in AI remains exceptionally high, and companies continue introducing AI into software development, customer service, marketing, and internal operations. Turning those experiments into measurable financial returns has proved more complicated. Research from MIT found most enterprise generative AI pilots produced little measurable improvement in financial performance, while Gartner reached a similar conclusion when evaluating organizations replacing parts of their workforce with AI agents, software that can complete multi-step tasks with limited human supervision. Companies often reported productivity gains, but those gains did not always translate into meaningful improvements in profitability.

None of this suggests that AI lacks real customers. It suggests the industry's investment cycle is running ahead of its revenue cycle, and that gap has become the focus of economists attempting to measure whether AI's financial foundations are keeping pace with its technological progress. Among them is Ed Yardeni, whose research compares the revenue generated by companies building AI models with the infrastructure spending required to support them. His conclusion is neither overtly optimistic nor pessimistic. The ecosystem is generating real revenue, but not yet enough end-user revenue to comfortably support the scale of investment flowing into it. The equation becomes much more favorable if revenue continues growing rapidly through the end of the decade and if the cost of computing keeps falling. Both assumptions are plausible, but neither is guaranteed.

Outperform the competition.

Tools & resources, ranging from playbooks, databases, courses, and more.

Deep dives on famous visionary leaders.

Interviews with entrepreneurs and playbook breakdowns.

*This is sponsored content

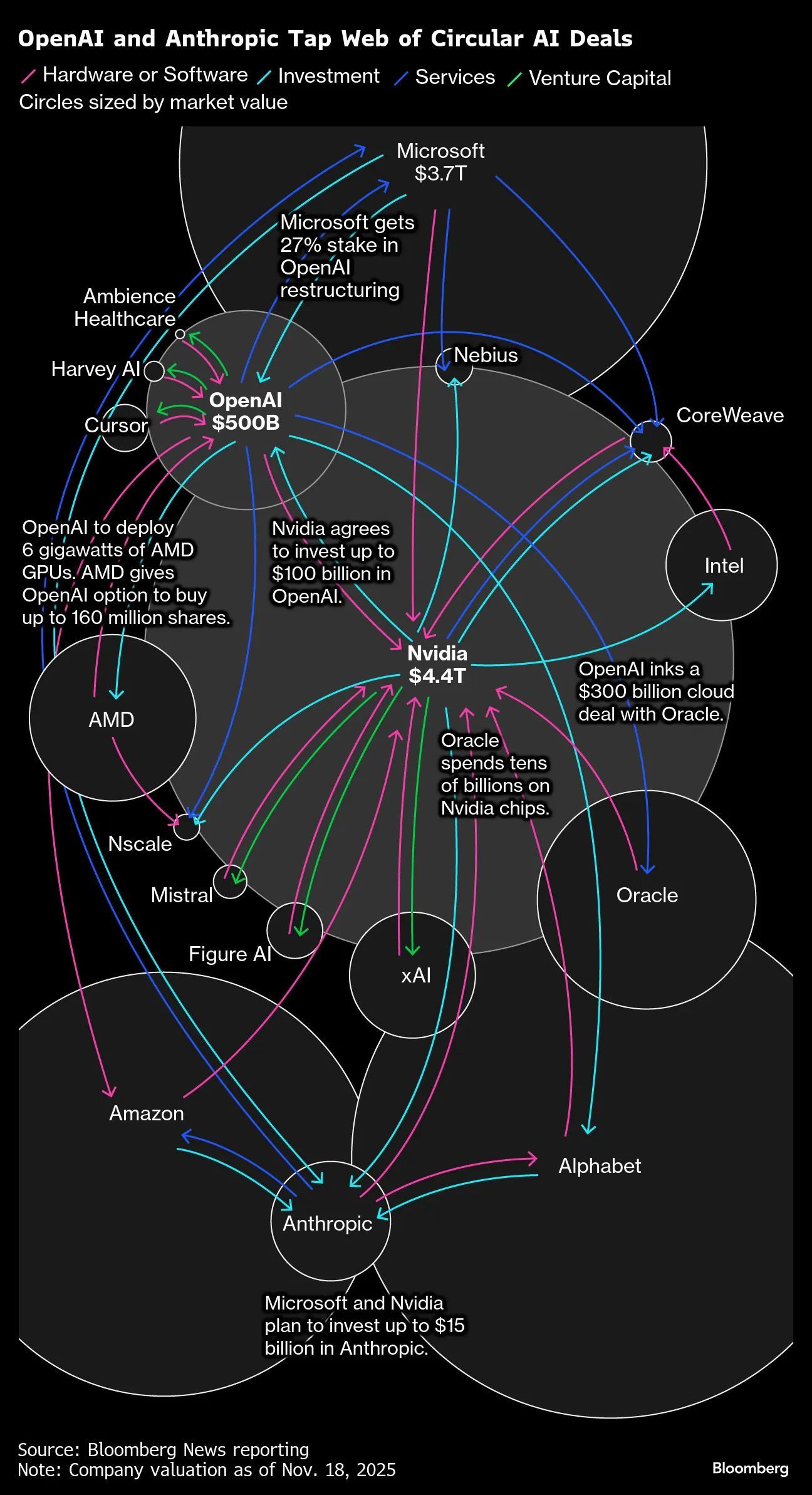

The AI money loop

The picture becomes more complicated because much of the money fueling today's AI boom circulates within the same small group of companies.

NVIDIA has invested heavily in OpenAI, and the ChatGPT maker has committed to purchasing substantial cloud computing capacity from Oracle and Amazon. Those cloud providers, in turn, buy NVIDIA's chips to build the infrastructure required to fulfill those contracts. Each transaction reflects genuine commercial activity, but the same dollar can appear multiple times as investment, backlog, infrastructure spending, and revenue as it moves through the ecosystem.

Critics describe the arrangement as a form of circular financing that can make demand appear broader than it really is. Supporters argue the opposite, saying these long-term agreements simply secure scarce computing resources before demand outstrips supply. The disagreement ultimately centers on one question: how much AI demand originates from customers outside this relatively small circle of technology companies?

Even reported profits have become harder to interpret, because AI infrastructure is unusually expensive and much depends on how companies account for the useful life of the hardware powering it. Most hyperscalers depreciate servers over five or six years, spreading their costs over that period. Some investors argue that the equipment becomes economically obsolete much sooner because each new generation of AI chips delivers significantly higher performance than the previous one. If servers effectively become outdated after only two or three years, depreciation expenses today may understate the true economic cost of maintaining AI infrastructure.

The debate is no longer theoretical. Amazon disclosed in a regulatory filing last year that revising the expected lifespan of some servers increased depreciation expense by hundreds of millions of dollars while reducing reported net income. The adjustment did not change Amazon's underlying business, but it illustrated how accounting assumptions can materially affect reported earnings at a time when companies are investing at unprecedented levels. Still, none of these accounting concerns make AI revenue imaginary.

Revenue exists, but timing matters

OpenAI and Anthropic have both reported annualized revenues measured in the tens of billions of dollars, making them among the fastest-growing software businesses ever created. Enterprises continue signing large contracts for AI services, developers are increasingly building applications around foundation models, and consumer products continue attracting new users. This means the commercial market clearly exists, but the challenge is one of timing rather than existence.

Building AI infrastructure requires enormous amounts of capital years before the corresponding revenue fully arrives. OpenAI alone has committed to infrastructure investments of hundreds of billions of dollars over the coming years, while acknowledging that profitability remains several years away. Similar dynamics exist across much of the industry. Companies are spending today based on expectations about customer demand several years into the future.

History offers both optimism and warning

That mismatch has invited comparisons with the internet boom of the late 1990s, although the parallels are often overstated. The internet ultimately transformed the global economy, but the investment cycle that built it also produced periods of excessive optimism, overbuilding, and painful market corrections before demand eventually caught up. Many companies disappeared. Others emerged as some of the most valuable businesses in history. The lesson is less about whether transformational technologies succeed than about whether capital is allocated at the right pace.

It is entering a similar phase of its development. The debate has shifted from technological capability to economic sustainability. Investors are no longer evaluating whether models can become more capable. They are increasingly evaluating whether customers can generate enough revenue to justify the infrastructure required to support those capabilities.

That distinction helps explain why June's market volatility mattered beyond a single week of trading. The AI economy has become tightly interconnected. Chipmakers depend on cloud providers. Cloud providers depend on AI labs, which in turn depend on enterprise customers and consumer subscriptions. Capital flows continuously between the same handful of companies, allowing the industry to expand with extraordinary speed while also making it more sensitive to disappointment at any point along the chain. A delayed data center, slower enterprise adoption, or weaker customer spending can quickly ripple through suppliers, infrastructure providers, and financial markets alike.

Few serious observers now argue that AI itself is a passing fad. The models continue to improve, businesses continue adopting them, and investment continues to flow into the sector. The more difficult question concerns timing. The industry is committing trillions of dollars to infrastructure today, even as demand is expected to mature later in the decade. If that demand arrives on schedule, today's spending may look prescient in the end. If it develops more slowly, the same financial machinery that accelerated the AI boom could amplify its growing pains.

That is the question investors began asking in June. It is also likely to shape the AI economy long after the market recovers from one volatile week.

P.S. Want to collaborate?

Share today’s news with someone who would dig it. It really helps us to grow.

Let’s partner up. Looking for some ad inventory? Cool, we’ve got some.

Deeper integrations. If it’s some longer-form storytelling you are after, reply to this email, and we can get the ball rolling.

What did you think of today's memo? |

|

.svg)

.svg)