Welcome to Memorandum Deep Dives. In this series, we go beyond the headlines to examine the decisions shaping our digital future. 🗞️

This week, we're tracking a company that, 18 months ago, looked like it belonged in the past tense. Intel, the firm whose name once sat inside nearly every PC on the planet, was bleeding billions, shedding tens of thousands of jobs, and watching its stock collapse. Few people were betting it would still matter much by the end of the decade.

Then the money started moving. The U.S. government took a stake. NVIDIA wrote a check. Apple, of all companies, came to the table. One by one, the biggest names in technology began to treat a wounded chipmaker as worth backing, and the market noticed.

So what changed? The answer has less to do with Intel's factories than with a single question hanging over the entire industry. Below, we trace how a near-bankrupt giant became one of the most closely watched bets in tech, and why its future may hinge on something nobody can fully predict yet.

In partnership with

LLM traffic converts 3× better than Google search

58% of buyers now start their research in ChatGPT or Gemini, not Google. Most startups aren't showing up there yet.

The ones that are get cited by the AI tools their buyers, investors, and future hires already use. And they convert at 3×.

A single point of failure

Somewhere in western Taiwan, on a strip of land smaller than most mid-sized cities, machines etch circuits onto silicon wafers that will eventually power almost every artificial intelligence system on Earth. The strip of land houses the foundry, a factory that manufactures chips designed by other companies, owned by TSMC.

The importance of Taiwan Semiconductor Manufacturing Company (TSMC) can be gauged by its grip on the global chip industry. As of 2025, TSMC commanded nearly 70% of the global foundry market, producing chips for Apple, NVIDIA, AMD, and Qualcomm. Its closest competitor, Samsung, held just 7.2%. That is less a competitive market than a dependency, and it sits at the center of one of the most volatile geopolitical fault lines on the planet.

The importance of TSMC further increased with the emergence of artificial intelligence and the technology’s reliance on high-end GPUs. Training and running modern AI systems require enormous numbers of advanced chips. And while companies like NVIDIA, AMD, Google, and Amazon may design those processors, nearly all are manufactured by TSMC. That means any disruption to Taiwan’s chip production, whether from geopolitical tensions, trade restrictions, or natural disasters, would reverberate throughout the AI industry with no immediate alternative.

That single vulnerability helps explain why Intel is probably the most viable Western alternative for advanced logic manufacturing at scale. The company that was on the verge of irrelevance 18 months ago is now at the center of a multi-billion-dollar effort to reshape where and how advanced chips get made.

From collapse to comeback

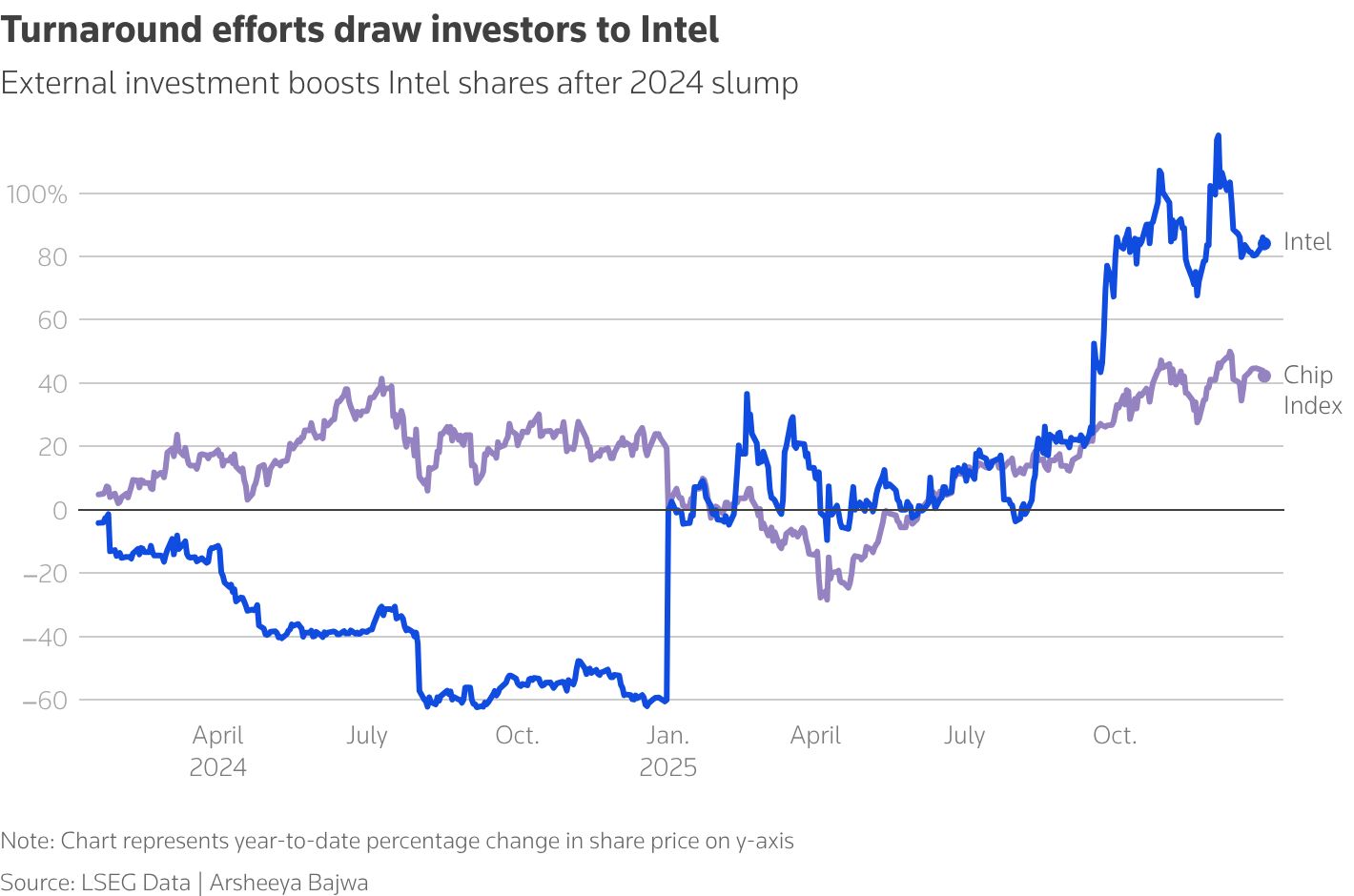

In mid-2024, Intel was in freefall, the company reported a $1.6B net loss, announced plans to eliminate 15k jobs, and suspended stock dividend for the first time in decades. Its manufacturing technology, once the global standard, had fallen behind TSMC by at least a generation, forcing its stock price to drop 60% over the year. As Intel’s competitive position deteriorated, CEO Pat Gelsinger resigned, and the company started working to regain its footing.

The company’s turnaround, to the extent there is one, began with Lip-Bu Tan’s appointment as CEO in March 2025. Tan, who had previously led chip design software firm Cadence Design Systems through a decade-long reinvention, did not waste time and cut roughly 21k more positions, roughly 20% of the remaining workforce, flattened a management structure he described as “eight or more layers deep,” and canceled planned factory projects in Germany and Poland. The goal was to shrink headcount from about 108,900 to approximately 75k by the end of 2025, a staggering compression for a company of Intel’s size.

At the same time, capital started flowing in from unexpected directions. The U.S. government converted its remaining CHIPS Act grants into an $8.9B equity stake, acquiring a 9.9% stake in the company. NVIDIA invested $5B and announced a partnership to co-develop custom processors for AI data centers and PCs, with Intel building x86 chips (the processor architecture that runs most of the world’s PCs and servers) and integrating them via NVIDIA's high-speed interconnect technology. For the first time in years, the narrative around Intel shifted from decline to something more provisional: a plausible reason to exist rather than a confirmed comeback.

Apple’s bet on Intel

On May 8, 2026, that plausibility grew considerably when Apple and Intel reached a preliminary agreement for Intel to manufacture some of the chips powering Apple devices. The two companies had been in intensive discussions for over a year, and early indications suggest the deal would initially cover lower-end processors, potentially including some chips used in iPads and Macs, with Intel fabricating them based on Apple’s own designs, much as TSMC does today.

The deal is significant because Apple is TSMC’s largest customer, and even a partial shift in production would signal that Apple now considers Intel’s manufacturing technology reliable enough for its products. The deal’s impact was immediate, and investors who believed Intel could pull off a turnaround sent its shares up nearly 14%.

The deal is also being viewed as validation of Intel’s new 18A chipmaking process and its advanced RibbonFET and PowerVia technologies.

Hire smarter with Athyna, save up to 70% on salary costs.

Athyna connects you with top LATAM AI talent, fast!

*This is sponsored content

The government’s $8.9B gamble

With these deals, Intel is evolving into something without a clear precedent: part chipmaker, part contract manufacturer, and part geopolitical asset owned in part by the U.S. government. And while ownership in itself does not make Intel a geopolitical asset, the deal between the U.S. government is structured so that Intel cannot spin off or sell its factories, tying the company’s future to national security priorities as much as to shareholder returns.

However, despite its shifting position, Intel’s future depends heavily on the path AI takes. The company’s change in fortunes relies on the assumption that AI will eventually spread beyond massive cloud data centers into enterprise servers, PCs, phones, and autonomous systems, requiring a broader mix of processors and more geographically diversified manufacturing. If that happens, Intel’s combination of chip design capabilities and domestic manufacturing capacity could make it one of the most strategically important companies in the American technology industry.

The financial picture shows both the promise and the risk of that strategy. Intel’s Q1 2026 revenue of $13.6B beat expectations, driven largely by growth in data center and AI businesses, and investor optimism has pushed the company’s valuation sharply higher. But the foundry division at the center of Intel’s long-term ambitions still lost $2.4B in the quarter, while free cash flow remained negative. Intel has also warned that if demand for its next-generation 14A manufacturing process fails to materialize, it could slow or stop future leading-edge development and rely on an external foundry for advanced chips.

The inference problem Intel can solve

And this is where Intel’s fate becomes inseparable from AI’s trajectory. Intel’s bet rests on the idea that AI will eventually move beyond the giant cloud data centers that dominate today’s market. Right now, most AI spending is concentrated on training large models like GPT or Gemini, workloads that depend heavily on NVIDIA’s GPUs packed into enormous server clusters. But once those systems are built, they still need to run continuously across offices, laptops, factory equipment, customer service systems, security cameras, cars, and phones.

That phase, known as inference, often relies less on massive GPU clusters and more on a wider mix of processors spread across ordinary computing infrastructure. A company deploying AI agents internally, for example, may not need thousands of top-end GPUs, but it will still require large numbers of CPUs and enterprise servers to manage databases, networking, security, storage, and day-to-day operations. Those are areas where Intel still has deep reach.

The same logic applies to AI PCs and edge devices. If AI systems increasingly run directly on laptops, industrial equipment, or mobile devices rather than exclusively in centralized cloud systems, demand shifts toward the kinds of processors Intel already manufactures at scale. In that scenario, Intel’s factories and product portfolio become more valuable because the AI economy would require not just a handful of hyperscale GPU providers, but a much broader computing foundation.

If that vision materializes, Intel’s product portfolio and its American factory network become genuinely strategic assets. If AI investment contracts, or if the highest-value work remains concentrated in GPU clusters and proprietary software ecosystems controlled by NVIDIA, Intel’s expensive manufacturing build-out could prove premature.

Intel’s current predicament reflects a broader shift in the tech sector: a technology that barely existed in mainstream consciousness three years ago is now reshaping industrial policy, redirecting tens of billions in government capital, and determining whether a 57-year-old chip company survives or becomes a footnote.

Intel did not set out to become a geopolitical instrument, but the AI boom has steadily pushed it into that role. Whether this transformation ultimately revives the company or simply prolongs an enormously expensive bet will depend on a question the entire industry is still struggling to answer: what AI eventually becomes, and how much infrastructure the world will ultimately need to support it.

P.S. Want to collaborate?

Share today’s news with someone who would dig it. It really helps us to grow.

Let’s partner up. Looking for some ad inventory? Cool, we’ve got some.

Deeper integrations. If it’s some longer-form storytelling you are after, reply to this email, and we can get the ball rolling.

What did you think of today's memo? |

|

.svg)

.svg)